Seems there is a counter-offer for the Belgian behemoth SABInBevCorp.

Tongue is firmly in cheek in this open letter from Lincoln’s Beard but it does strike at where craft beer is different and why I think it is better.

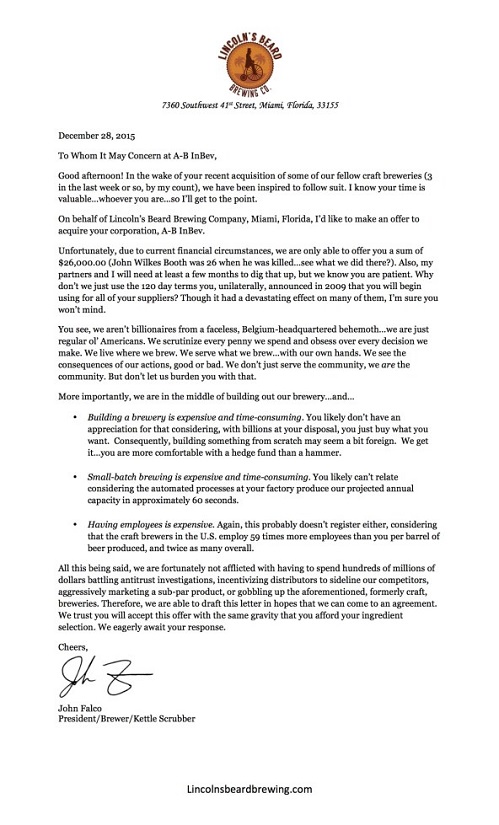

With a B?

I had to rub my eyes when I saw the number. Without any coffee in my system, I was sure that I had mis-read it. But I had not there was a “B” not an “M” next to the ..illion in the news that Constellation Brands would acquire Ballast Point Brewing for $1 billion (give or take).

Here is the back story on the buyer: Constellation ranks third big beer wise on the strength of imported brands such as Corona Extra, Corona Light, Modelo Especial, Negra Modelo and Pacifico. They are also in the wine business, as owners of Robert Mondavi, Clos du Bois, and others. They also are in the spirits game with SVEDKA Vodka and Black Velvet Canadian Whisky.”

With so many mergers and acquisitions this year, reactions have become predictable. It is clear by now that if you sell to someone who produces good beer or you sell only a partial stake, your brewery will not be smudged with bad PR residue. Private Equity (good or bad) gets more of a pass than ABInBev ever will. In this case the stink of Corona combined with the full sale and that high price will garner more negative than positive Google searches for the next few weeks.

With every deal there are both good and bad. The most exciting or damaging aspects might not appear for months or years but here are my knee-jerk reactions to the sale.

On the positive side, considering that Ballast Point distills spirits as well, the new owners will understand both markets which must have been a plus for both. Also, now that the pockets are deeper the expansion may increase in more brewing capacity and larger distribution even though they have been expanding their presence all over San Diego with tasting rooms and restaurants like the huge location in Little Italy that I was impressed by.

Flipping the coin, does Constellation know how to sell craft beer or will they really leave that to Ballast Point? What kind of pressure will Ballast Point be under to perform up to the standards of the price set?

The largest negative in the near term is the public perception. Some breweries have either a great product (Bourbon County Stout for Goose Island) or great brewers that are respected (10 Barrel with Tonya Cornett for one) that brings people back into the fold. Sculpin and their Victory at Sea variants along with the spirits line should assuage some harsher feelings to Ballast Point in a way that hasn’t happened for the likes of Elysian (divided ownership/lost brewmaster) or Golden Road (who reinforced a feeling of embracing big and average that has dogged it from the start).

Stepping back from the tree to the forest, that someone would pay this much money for a brewery either shows that it was in high demand and that the bidding pushed its valuation every higher or that Constellation really, really wanted Ballast Point and that the price wasn’t too high to stop them. Which to me means, that they think it is still a good economic play. They might have been able to buy another import to add to their portfolio with the “big” merger causing spin offs but Constellation wanted in to craft beer.

That might be the biggest take-away from this. Business now sees craft beer as potential and they are opening their wallets too.